Mobile App Architecture for FinTech Apps (Security + Scaling)

TL;DR

- Swift enables fast, secure, and high-performance iOS app development

- Builds scalable apps tailored for the Apple ecosystem

- Delivers superior UX, reliability, and data security

- Ideal for startups and enterprises targeting premium users

- Supports seamless integration across Apple devices and platforms

What happens when millions of users try to make a payment at the same moment and your app crashes for just five minutes?

In the FinTech world, that’s not a small issue. It leads to lost revenue, broken trust, and potential regulatory risk. Users don’t see technical failures; they see a platform they can’t rely on.

As the FinTech market moves toward a $1 trillion+ valuation, the demand for fast, secure, and always-available mobile apps is growing rapidly. Today, financial transactions are increasingly mobile-first, and users expect instant processing, seamless experiences, and bank-grade security every time.

But delivering this is complex. FinTech apps must manage real-time transactions, sensitive data, heavy user loads, and strict compliance requirements, all without compromising performance. Even minor delays or vulnerabilities can lead to serious consequences.

This is why mobile app architecture is a critical business decision, not just a technical one. The right approach ensures scalability, security, and adaptability in a fast-evolving ecosystem.

Modern FinTech apps rely on cloud-native, microservices-based architectures with secure APIs, enabling them to scale efficiently while maintaining performance and compliance.

In this blog, we’ll explore how to build FinTech architectures that balance security, scalability, and user trust.

What Is Mobile App Architecture?

Mobile app architecture is the structural framework that defines how different components of an application interact to process user inputs, manage data, and deliver outputs efficiently.

It acts as the foundation of an application, determining how its frontend, backend, APIs, and databases work together. It outlines the system’s structure, data flow, and communication patterns that ensure the app functions smoothly under different conditions.

In simple terms, it is the blueprint that guides how an app is built, scaled, and maintained over time.

A well-designed architecture ensures that an application can handle real-world challenges such as increasing user demand, data complexity, and performance expectations. It also enables seamless integration with third-party services like payment gateways, identity verification systems, and analytics tools especially critical in FinTech applications.

It is important to distinguish between architecture and tech stack. While architecture defines how the system is structured and operates, the tech stack refers to the specific technologies used to implement that structure, such as programming languages, frameworks, and cloud platforms.

Key Insight

Mobile app architecture is not just about how an app is built. It is about how well it performs, scales, and adapts as your business grows.

Why Is Mobile App Architecture Important?

A well-designed mobile app architecture is essential to create robust, scalable, and user friendly applications. It offers several benefits that contribute to app’s success.

Firstly, it enhances modularity, allowing different components to be developed and maintained independently, leading to easier updates and modifications. For instance, in an e-commerce app, a modular architecture enables seamless integration of new payment gateways without affecting other functionalities.

Secondly, robust security measures in the architecture ensure data protection and prevent unauthorized access. A banking app, for instance, can be fortified with encryption protocols and secure authentication methods, instilling trust among users and safeguarding their sensitive information.

Moreover, reliability is heightened as a well-structured architecture minimizes bugs and errors, providing users a seamless experience. Think about a message app that rarely crashes or experiences glitches due to its meticulously designed architecture.

Furthermore, performance and scalability are optimized, allowing the app to handle increasing user loads and adapt to growing demands over time. An example is a social media platform capable of accommodating millions of users concurrently without compromising speed or functionality.

Layers of Mobile Application Architecture

Most mobile app architectures have three layers: presentation, business, and data.

- Presentation Layer

The presentation layer, or front end, is the user interface (UI) you see when opening an app. It includes the screens, navigation, controls, and visual elements. For example, in a messaging app like WhatsApp, the presentation layer comprises chat screens, contact lists, setting menus, etc.

Its primary function is to enable user interaction by taking input from users and displaying output from the lower layers.

- Business layer

The business layer contains the core applications logic that handles tasks like sending and receiving messages, encrypting data, detecting spam, managing notifications, etc. It takes input from the presentation and data layers, processes it, and prepares the responses displayed in the UI.

- Data Layer

The data layer abstracts the physical storage, so other layers don’t need to worry about the specifics of data bases. It handles queries, connections, coaching, concurrency, and other data access mechanisms. The business layer interacts with the data layer by calling methods it exposes.

What is the Core Architecture and Technical Infrastructure of FinTech Apps?

Quick Answer

FinTech apps are built on cloud-native, microservices-based architectures supported by secure APIs, scalable databases, and resilient infrastructure. This combination enables them to process high volumes of financial transactions in real time while maintaining strong security and compliance.

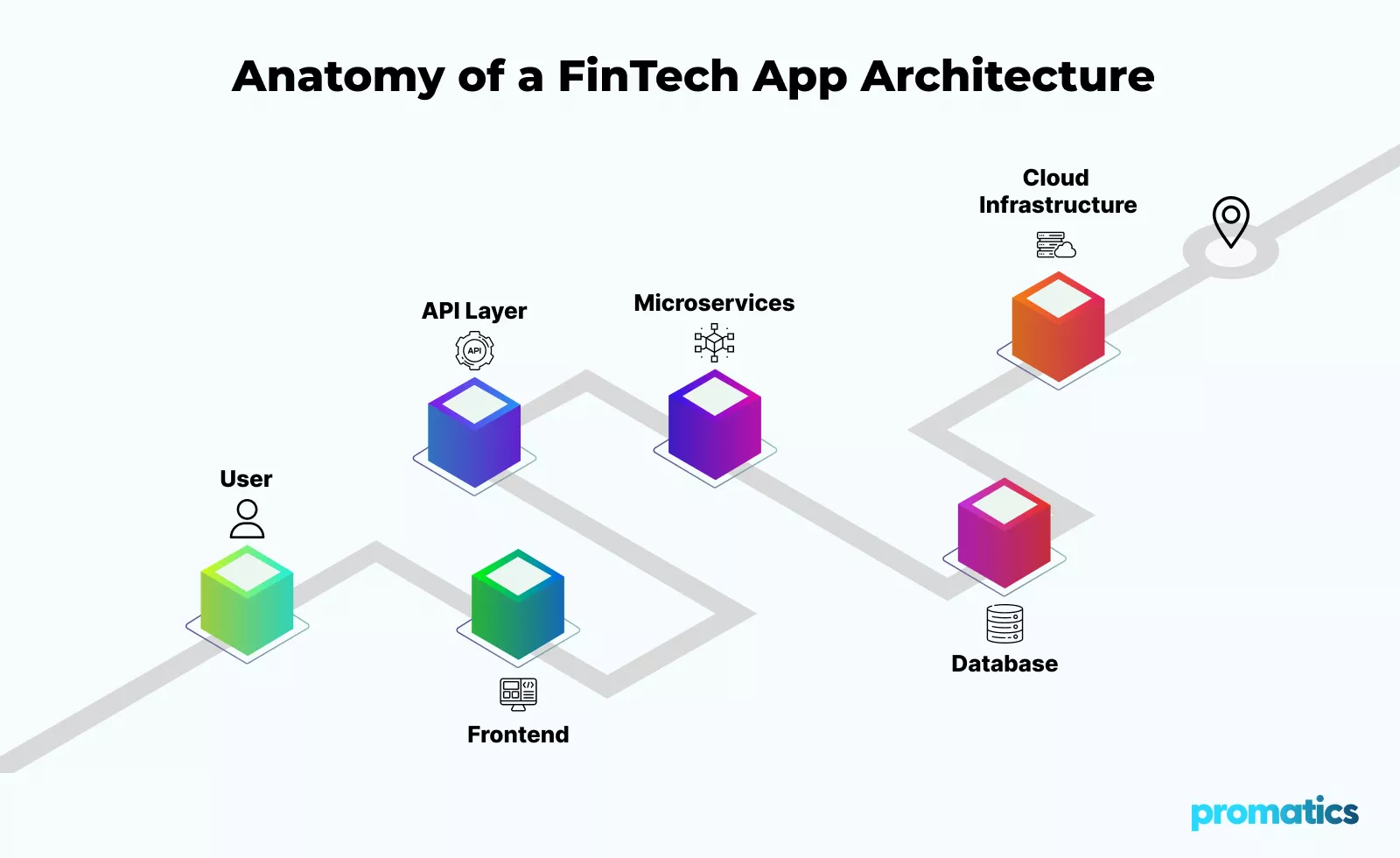

Key Components of FinTech Architecture

A modern FinTech application is not a single system but a layered ecosystem where each component plays a critical role in ensuring performance, scalability, and reliability.

1. Frontend Layer (User Interface)

The frontend is the user-facing side of the application and directly impacts user experience and retention.

- Built using technologies like Flutter, React Native, Swift, or Kotlin

- Designed for speed, responsiveness, and simplicity

- Supports features such as biometric authentication, real-time transaction updates, and intuitive dashboards

- Optimized for multiple devices and screen sizes

A seamless frontend ensures users can perform financial actions quickly and confidently.

2. Backend Layer (Application Logic)

The backend acts as the brain of the application, handling all business logic and operations.

- Built using microservices architecture, where each service performs a specific function

- Examples include payment processing, user authentication, fraud detection, and notifications

- Enables independent scaling and deployment, reducing system downtime

- Improves fault isolation so one service failure does not impact the entire system

This modular approach is essential for handling the complexity of financial systems.

3. API Layer (Integration Hub)

APIs are the backbone of FinTech connectivity, enabling seamless communication between systems.

- Integrates with banks, payment gateways, KYC providers, and third-party services

- Uses RESTful or GraphQL APIs for efficient data exchange

- Secured using protocols like OAuth 2.0 and token-based authentication

- Enables open banking and ecosystem-driven innovation

Without APIs, FinTech apps cannot function in today’s interconnected financial landscape.

4. Database Layer

FinTech apps deal with both structured and high-velocity transactional data, requiring a hybrid approach.

- SQL databases for structured financial records and compliance

- NoSQL databases for scalability and real-time data handling

- Use of distributed databases ensures high availability and fault tolerance

- Supports data replication and backup for reliability

Efficient database design ensures accuracy, consistency, and speed in financial operations.

5. Cloud and Infrastructure Layer

Cloud infrastructure provides the foundation for scalability and resilience.

- Hosted on platforms like AWS, Microsoft Azure, or Google Cloud

- Uses containerization (Docker) and orchestration (Kubernetes) for efficient resource management

- Enables auto-scaling, ensuring the app can handle sudden traffic spikes

- Implements load balancing to distribute requests evenly

- Supports multi-region deployment for high availability and disaster recovery

Cloud-native infrastructure allows FinTech apps to grow without performance bottlenecks.

Architecture Comparison

| Architecture Type | Advantages | Limitations | Best Use Case |

| Monolithic | Simple development and deployment | Difficult to scale and maintain | MVPs and small apps |

| Microservices | High scalability and flexibility | Requires complex management | Large-scale FinTech platforms |

| Serverless | Cost-efficient and event-driven | Limited control over infrastructure | Lightweight, event-based features |

Best Practices for Core Infrastructure

- Use API gateways for centralized traffic and security management

- Implement load balancers to handle high user traffic efficiently

- Enable auto-scaling to maintain performance during peak usage

- Adopt CI/CD pipelines for faster and safer deployments

- Ensure end-to-end encryption across all layers

- Monitor systems in real time using observability tools

How Do Different FinTech Architectures Compare?

Quick Answer:

Different FinTech architectures vary in scalability, flexibility, and complexity, with microservices architecture offering the best balance for modern, high-growth applications.

Choosing the right architecture is a critical decision in FinTech development. Each architectural model comes with its own advantages and trade-offs, depending on factors such as application scale, performance requirements, and long-term growth plans.

Below is a comparison of the most commonly used architectures in FinTech:

| Architecture | Advantages | Limitations | Best Use Case |

| Monolithic | Simple to develop and deploy, easier for small teams | Difficult to scale, tightly coupled components | MVPs and small applications |

| Microservices | Highly scalable, flexible, better fault isolation | Requires complex management and orchestration | Large-scale FinTech platforms |

| Serverless | Cost-efficient, event-driven, auto-scaling | Limited control over infrastructure, vendor dependency | Lightweight and event-based features |

Key Differences Explained

Monolithic Architecture

In a monolithic setup, all components are built and deployed as a single unit. While this approach simplifies initial development, it becomes challenging to scale and maintain as the application grows.

Microservices Architecture

Microservices divide the application into smaller, independent services. Each service handles a specific function, such as payments, authentication, or notifications. This enables better scalability, faster updates, and improved system resilience.

Serverless Architecture

Serverless architecture allows developers to run code in response to events without managing infrastructure. It is highly efficient for specific use cases but may not be suitable for complex, large-scale FinTech systems requiring full control.

Key Insight:

For most modern FinTech applications, microservices architecture is preferred because it enables independent scaling of critical services, improves system reliability, and supports continuous innovation.

What Regulatory Compliance Frameworks Apply to FinTech Apps?

Quick Answer

FinTech apps must comply with financial regulations, data privacy laws, and payment security standards based on the regions they operate in. These regulations ensure secure transactions, protect user data, and maintain the integrity of financial systems.

Why Compliance is Critical in FinTech

FinTech applications operate in a highly regulated environment because they deal with sensitive financial data, digital payments, and user identities. Unlike other mobile apps, even a small compliance gap can lead to serious consequences.

Failure to comply can result in:

- Significant financial penalties and legal actions

- Suspension or revocation of operational licenses

- Increased risk of fraud and cyberattacks

- Loss of customer trust and brand reputation

More importantly, compliance builds credibility and trust, which are essential for user adoption in financial services.

Key Regulations and Standards

FinTech companies must follow multiple frameworks depending on their geography, product type, and target audience:

- PCI DSS (Payment Card Industry Data Security Standard)

Ensures secure processing, storage, and transmission of cardholder data. It is mandatory for any app handling card payments. - GDPR (General Data Protection Regulation)

Applies to businesses dealing with EU users. It governs how personal data is collected, stored, and processed, with strict rules on user consent and data rights. - RBI Guidelines (Reserve Bank of India)

Covers digital payments, data localization, KYC norms, and licensing requirements for payment aggregators, wallets, and NBFCs in India. - KYC (Know Your Customer) & AML (Anti-Money Laundering)

Require identity verification and continuous monitoring to prevent fraud, terrorism financing, and illegal financial activities. - PSD2 (Payment Services Directive 2)

Encourages open banking and secure third-party integrations in Europe.

Licensing Requirements

FinTech apps often need specific licenses depending on their services and region of operation. These may include:

- Payment Aggregator or Payment Gateway licenses

- NBFC (Non-Banking Financial Company) licenses for lending platforms

- Digital wallet approvals

- Banking or financial institution partnerships

Licensing determines what services a FinTech app can legally offer and ensures adherence to regulatory frameworks.

Compliance Checklist

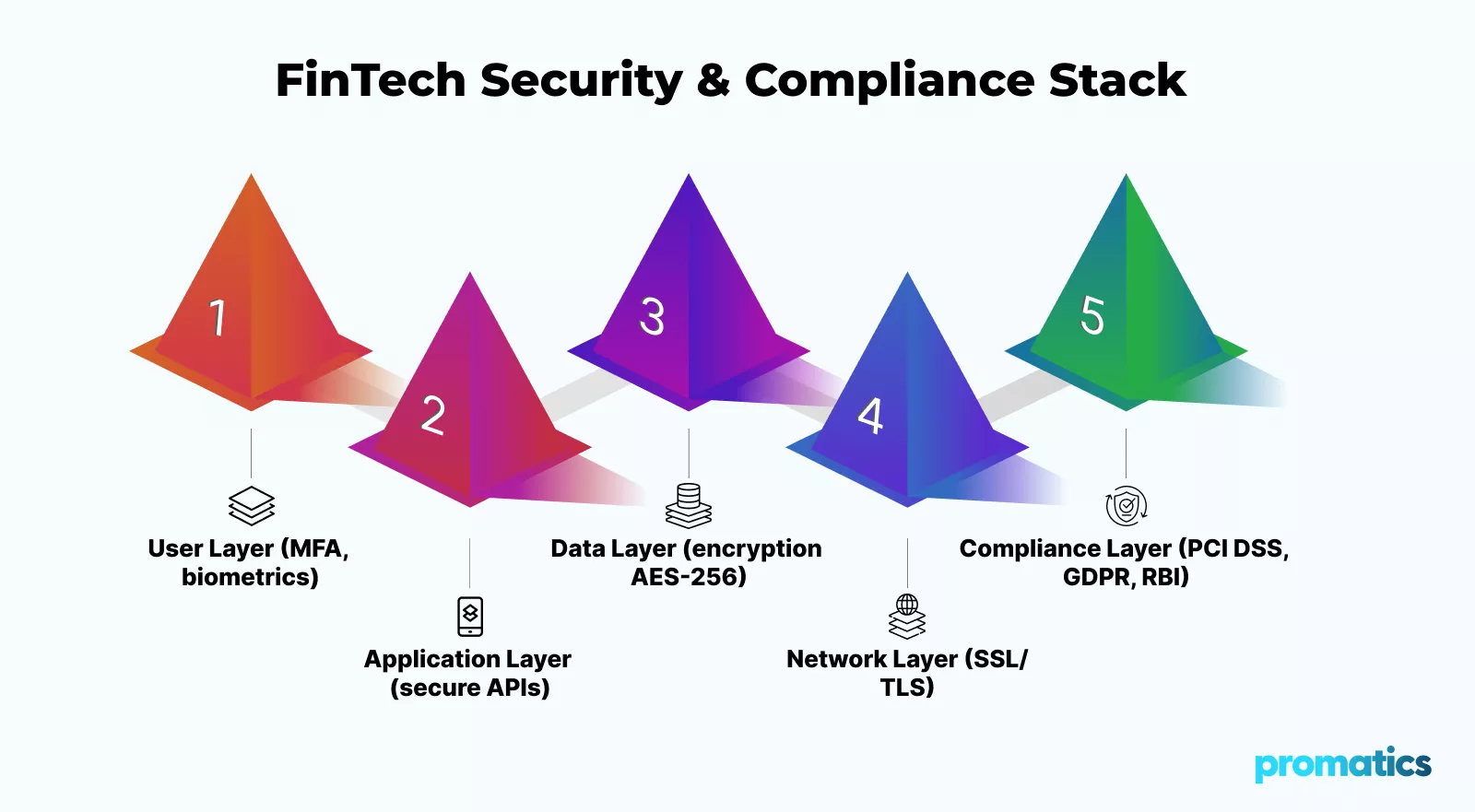

To meet regulatory requirements, FinTech apps must implement strong security and governance measures:

- Data Encryption

Protect sensitive data using encryption standards like AES-256 for storage and SSL/TLS for transmission - Secure Authentication

Use multi-factor authentication (MFA), biometrics, and secure login mechanisms - Audit Logs and Monitoring

Maintain detailed records of transactions and user activities for transparency and audits - Regular Security Testing

Conduct penetration testing, vulnerability assessments, and security audits - Data Privacy Controls

Provide clear consent mechanisms and allow users to manage their data - Fraud Detection Systems

Use AI-based monitoring to identify suspicious activities in real time

Best Practices for Staying Compliant

- Integrate compliance into the architecture from the beginning, not as an afterthought

- Use RegTech tools to automate compliance monitoring and reporting

- Stay updated with changing regulations across regions

- Conduct regular internal and external audits

- Train teams on data security and compliance protocols

How Can User Experience Optimization and Personalization Be Achieved?

Quick Answer

Use AI, behavioral analytics, and intuitive UI design to deliver personalized and seamless user experiences.

UX Best Practices

- Minimal onboarding steps

- Biometric login (Face ID, fingerprint)

- Real-time notifications

- Simplified dashboards

Personalization Techniques

- AI-based spending insights

- Smart recommendations

- Custom alerts

Impact on Business

- Higher retention rates

- Increased engagement

- Better customer trust

How Do Different FinTech Architectures Compare?

Quick Answer

Microservices outperform monolithic systems in scalability, resilience, and faster innovation cycles.

Comparison Table

| Feature | Monolithic | Microservices |

| Scalability | Low | High |

| Deployment | Slow | Fast |

| Fault Isolation | Poor | Strong |

| Maintenance | Difficult | Easier |

Key Insight

Microservices enable independent scaling of critical services like payments and authentication.

What Risk Management and Security Protocols Are Essential?

FinTech apps require multi-layered security, including encryption, fraud detection, and continuous monitoring.

Security Layers

- Data Encryption (AES-256, SSL/TLS)

- Authentication (MFA, biometrics)

- Fraud Detection Systems

- Secure APIs

Risk Management Strategies

- Real-time transaction monitoring

- AI-based anomaly detection

- Regular penetration testing

Common Threats

- Data breaches

- Phishing attacks

- API vulnerabilities

What Are the Emerging Trends and Future Developments in FinTech Architecture?

Future FinTech applications will be driven by advanced technologies such as artificial intelligence, blockchain, and embedded finance, enabling faster, more secure, and highly personalized financial experiences.

Key Trends

AI & Machine Learning

Artificial Intelligence (AI) and Machine Learning (ML) are transforming how financial systems operate. These technologies enable real-time data analysis, predictive modeling, and intelligent automation.

- AI-powered fraud detection systems can identify suspicious transactions instantly

- Personalized financial insights based on user behavior and spending patterns

- Chatbots and virtual assistants for 24/7 customer support

- Automated credit scoring and risk assessment

As AI continues to evolve, FinTech apps will become more proactive rather than reactive, anticipating user needs before they arise.

Blockchain for Secure Transactions

Blockchain technology introduces decentralized, tamper-proof systems that enhance transparency and security.

- Enables secure peer-to-peer transactions without intermediaries

- Reduces fraud through immutable transaction records

- Powers smart contracts for automated financial agreements

- Enhances cross-border payments with faster settlement times

This technology is particularly valuable in reducing operational costs and increasing trust in financial ecosystems.

Open Banking APIs

Open banking is reshaping how financial services are delivered by allowing secure data sharing between institutions.

- Enables third-party integrations with banks and financial services

- Supports ecosystem-driven innovation and partnerships

- Improves customer experience through unified financial platforms

- Encourages competition and faster product innovation

APIs act as the backbone of this transformation, making financial services more interconnected and accessible.

Embedded Finance

Embedded finance integrates financial services directly into non-financial platforms.

- Enables in-app payments, lending, and insurance

- Creates seamless user experiences without switching platforms

- Expands financial access across industries like eCommerce and SaaS

- Drives new revenue streams for businesses

This trend is rapidly blurring the lines between financial and non-financial services.

Voice-Enabled Banking

Voice technology is emerging as a new interface for financial interactions.

- Allows users to perform transactions using voice commands

- Enhances accessibility for non-tech-savvy users

- Integrates with smart devices and virtual assistants

- Provides faster and more convenient banking experiences

As natural language processing improves, voice banking is expected to become more secure and widely adopted.

Future Outlook

Hyper-Personalized Financial Services

FinTech apps will leverage AI and big data to deliver highly customized experiences.

- Tailored investment strategies

- Personalized budgeting and saving recommendations

- Dynamic financial dashboards based on user behavior

This level of personalization will significantly improve user engagement and loyalty.

Fully Automated Financial Decision-Making

Automation will reduce human intervention in financial processes.

- Robo-advisors managing investments

- Automated lending decisions using AI models

- Smart financial planning tools

This will make financial services faster, more efficient, and accessible to a broader audience.

Increased Adoption of RegTech (Regulatory Technology)

As regulations become more complex, RegTech solutions will play a critical role.

- Automates compliance monitoring and reporting

- Reduces risk of regulatory violations

- Enhances transparency and audit readiness

- Enables real-time compliance tracking

RegTech will become a core component of FinTech architecture rather than an add-on.

How Promatics Technologies Builds Scalable FinTech Architectures

Promatics Technologies designs and implements scalable, secure, and high-performance mobile app architectures tailored for FinTech applications, ensuring reliability, compliance, and long-term growth.

In the FinTech ecosystem, architecture is not just a technical layer, it is the foundation that determines how well an application performs under real-world conditions. From handling high transaction volumes to ensuring data security and regulatory compliance, every architectural decision directly impacts business success.

At Promatics Technologies, mobile app architecture is approached strategically, combining technical expertise with business alignment. Instead of relying on generic frameworks, architectures are designed based on specific product requirements, user behavior, and scalability goals.

This ensures that applications are not only functional but also resilient, secure, and future-ready.

1. Scalable Application Architecture

Promatics builds cloud-native systems designed to handle growing user demand and real-time financial transactions without performance degradation.

- Auto-scaling infrastructure to manage traffic spikes

- Load balancing for optimal resource utilization

- Distributed systems for high availability

This ensures uninterrupted performance, even during peak transaction loads.

2. Microservices-Based Development

Applications are structured using microservices, enabling modular and independent service execution.

- Faster feature releases and updates

- Strong fault isolation to minimize system-wide impact

- Independent scaling of critical services

This approach supports agility and continuous innovation in complex FinTech environments.

3. Secure Backend and API Infrastructure

Security is integrated into every layer of the architecture to protect sensitive financial data.

- Secure API frameworks using OAuth and token-based authentication

- End-to-end encryption for data in transit and at rest

- Robust identity and access management systems

This ensures compliance with global security standards while building user trust.

4. Cloud and DevOps Integration

Promatics leverages modern cloud platforms and DevOps practices to enhance system performance and deployment efficiency.

- Deployment across AWS, Azure, and Google Cloud

- CI/CD pipelines for faster and reliable releases

- Containerization with Docker and orchestration using Kubernetes

This enables continuous delivery, reduced downtime, and improved system reliability.

5. Cross-Platform and Native Development

Architecture decisions are aligned with performance requirements and business goals.

- Native development using Swift (iOS) and Kotlin (Android)

- Cross-platform development using Flutter and React Native

This ensures the right balance between performance, scalability, and cost efficiency.

6. UI/UX-Aligned Architecture

User experience is deeply integrated into architectural decisions.

- Fast-loading interfaces with minimal latency

- Real-time data synchronization for instant updates

- Seamless navigation across app workflows

This directly contributes to higher engagement and user retention.

7. AI and Advanced Technology Integration

Promatics incorporates advanced technologies to enhance application intelligence and automation.

- AI-driven personalization and recommendations

- Predictive analytics for smarter financial insights

- Automation through chatbots and intelligent workflows

This enables FinTech applications to deliver more personalized and efficient user experiences.

Why Businesses Choose Promatics Technologies

- Proven expertise in building scalable FinTech and enterprise applications

- Strong focus on security, compliance, and performance

- End-to-end capabilities from architecture design to deployment and scaling

- Deep experience in cloud, AI, and modern mobile technologies

Promatics Technologies helps build the core architecture of your FinTech application in a way that ensures it remains fast, secure, and scalable no matter how your business grows.

Conclusion

Building a successful FinTech application today is not just about launching features. It is about creating systems that can evolve with changing user expectations, regulatory landscapes, and technological advancements. The difference between an app that scales and one that struggles often comes down to how well its foundation is designed from the start.

As financial ecosystems become more interconnected and the demand for real-time, secure experiences continues to grow, businesses need to think beyond short-term development and focus on long-term architectural resilience.

This is where the right expertise makes a measurable difference.

If you are planning to build or scale a FinTech application, partnering with an experienced team like Promatics Technologies can help you translate complex architectural requirements into scalable, secure, and future-ready solutions.

Ready to build a FinTech app that performs reliably at scale? Connect with Promatics Technologies to explore how the right architecture can accelerate your product’s growth and long-term success.